Insurance vs. body shop estimates often leave drivers confused after a car accident. You expect your insurer to cover the cost of repairs, but their estimate rarely matches the one from a certified body shop—and the shop’s quote is usually higher. This blog breaks down why these differences happen, what they mean for your repair, and how to make sure you get the right fix for your vehicle.

Why Are Insurance Estimates Often Lower?

When comparing insurance vs. body shop estimates, the difference usually comes down to priorities. Insurance adjusters work on behalf of the insurance company and are primarily focused on keeping claim costs within a specific budget—not necessarily on ensuring the most complete or safest repair. As a result, their estimates often fall short of what certified body shops determine is actually needed. To understand why, let’s take a closer look at what causes this pricing gap:

1. Standardized Pricing Tools

For starters, insurance adjusters frequently use estimating software such as Audatex, CCC ONE, or Mitchell to produce repair quotes. These tools are designed for speed and consistency, using preset formulas and national averages to streamline the process.

However, this approach often overlooks important local factors. It typically fails to reflect regional labor rates, real-time OEM parts pricing, or the specific structural and electronic complexities of your vehicle. As a result, the first major gap in insurance vs. body shop estimates begins with a one-size-fits-all pricing model that doesn’t match the real-world cost of safe, certified repairs.

A 2023 report by CCC Intelligent Solutions showed that automated estimates based on national averages missed necessary operations in over 35% of reviewed cases. Source: CCC Intelligent Solutions Crash Course Report, 2023

2. Quick Inspections

Many insurers now rely on “virtual estimates,” asking you to submit photos of the damage instead of inspecting your vehicle in person. While convenient, these quick, surface-level reviews often miss hidden issues—especially in newer, tech-equipped vehicles.

This shortcut creates a major gap in insurance vs. body shop estimates. Certified shops perform full teardowns that reveal problems insurance adjusters routinely overlook, including:

-

Bent or cracked frame rails

-

Dislodged sensors (especially in ADAS-equipped vehicles)

-

Hidden suspension or structural damage

A 2022 study by Mitchell International found that over 70% of photo-based insurance estimates required supplementsonce shops uncovered additional damage.

3. Cheaper Parts and Labor

Insurance estimates and body shop quotes often differ significantly. This discrepancy isn’t accidental—in fact, it stems from how insurers calculate repair costs compared to what certified shops actually charge.

-

OEM vs. Aftermarket: Not All Parts Are Equal

To cut expenses, many insurance companies choose aftermarket, recycled, or remanufactured parts over OEM (Original Equipment Manufacturer) parts. While this reduces the total estimate, it often compromises quality.

For example, aftermarket parts may not align precisely with the vehicle’s original specifications. As a result, you might experience issues with panel alignment, ADAS system calibration, or paint matching.

According to the Property Casualty Insurers Association (2022), OEM parts can cost 25–75% more than aftermarket parts, depending on the type and make.

Source: PCI Research Brief (2022)

-

Labor Rates: The Hidden Cost Gap

In addition to cheaper parts, insurers often base labor costs on discounted rates from DRP (Direct Repair Program) shops. These rates do not reflect the actual prices that most skilled technicians charge—especially in California’s metro areas.

In contrast, certified and independent repair facilities charge market-based rates that account for regional cost differences, advanced training, and specialized tools.

Source: California Department of Insurance Labor Rate Survey, 2023

-

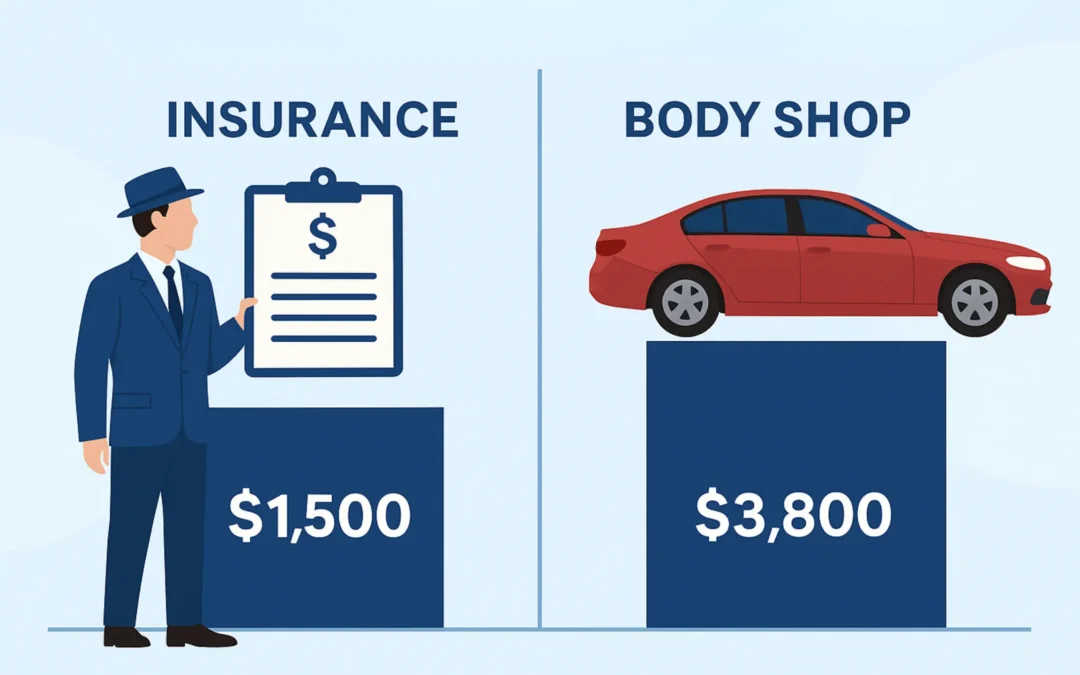

Estimate Disparities

The following chart shows just how much insurer estimates can differ from body shop estimates: As you can see, insurance-based estimates often fall below $1,500, while body shop assessments commonly exceed $3,800—a gap of more than $2,300.

This bar graph illustrates the average cost difference between insurance adjuster estimates and certified body shop estimates. On average, certified shops quote significantly higher—but more accurate—repair costs because they include hidden damage and OEM procedures.

4. Why This Matters

If you rely only on your insurance estimate, you might not get the full repairs your vehicle needs. This cost gap can lead to:

-

Out-of-pocket expenses

-

Delayed or incomplete repairs

-

Safety risks due to cheaper parts or rushed labor

To avoid these problems, make sure your repair quote includes OEM parts and real labor rates. If something seems too low, there’s probably a reason—and it’s worth asking questions.

Why Body Shop Estimates Are More Accurate

Certified body shops are focused on doing the job right—not just meeting a quota. Their estimates tend to be more comprehensive because they reflect the actual work required to restore your vehicle to pre-accident condition. Here’s why:

1. Detailed Inspections

Unlike photo-based or quick walk-around reviews done by insurance adjusters, body shops do full teardowns. This allows them to:

- Find hidden structural or mechanical damage

- Check alignment and safety systems

- Perform pre-repair diagnostic scans

According to CCC Intelligent Solutions, body shops discover additional damage in more than 60% of initial insurance-reviewed claims once they begin teardown and scanning.

This graph shows how much more damage is found during a full teardown at a body shop versus what an adjuster typically sees in a surface-level or photo inspection. It’s a clear reminder of why in-depth inspections matter.

2. OEM Parts and Procedures

Shops with OEM certifications from brands like Tesla, Porsche, or Mercedes-Benz are required to follow specific manufacturer repair procedures. These include:

- Using factory-approved parts and materials

- Following structural repair protocols

- Performing safety system recalibrations

This ensures that all repairs meet the same safety and quality standards as the original vehicle build.

3. Full Repair Plans

Certified shops don’t just list surface fixes. Their estimates account for:

- ADAS recalibrations (lane assist, cameras, sensors)

- OEM paint color matching

- Welds, frame pulls, corrosion protection, and post-repair scans

Mitchell International reports that certified repair centers include an average of 25–35 more line items per estimate than insurer-preferred shops.

Real Example: Estimate Comparison

Let’s look at a real-world comparison to show how far apart insurance and body shop estimates can be.

In this case, a driver was rear-ended at a stoplight. The damage appeared minor at first glance, and the car remained drivable. The insurance company issued a virtual estimate based on submitted photos. However, once the car was brought to a certified collision center, a full teardown revealed extensive hidden damage.

This chart highlights the common cost increase between an initial insurance estimate and the final approved repair cost after supplements. It visualizes how often repairs are underwritten at first and corrected only after further inspection.

This type of discrepancy is common. According to CCC Intelligent Solutions’ 2024 report, over 63% of repairs involve a supplemental claim, and the average gap between the insurer’s initial estimate and the final approved repair cost is $1,200–$1,800.

Source: CCC Intelligent Solutions, 2024 Industry Analysis

What Is a Supplemental Claim?

A supplemental claim is a formal request submitted by the body shop to your insurance company when additional damage is discovered after the initial estimate. In modern collision repair, this is no longer unusual—it’s the industry norm.

According to CCC Intelligent Solutions’ 2024 report, 63% of collision repairs require at least one supplement, with many involving two or more. These claims often address damage or procedures that weren’t included in the original estimate, such as:

-

Damage hidden beneath exterior panels during the initial inspection

-

Items overlooked or underestimated in the insurance company’s first assessment

-

Issues that only become clear after diagnostic scans or part removal

Common Reasons for Supplements

Several factors can lead a shop to file a supplemental claim:

-

Structural problems like bent frame rails or crushed crumple zones

-

Calibration needs for safety features such as ADAS, lane assist, or blind spot monitoring

-

Mechanical concerns affecting suspension or steering uncovered during disassembly

-

Additional OEM-specific steps required for safe, compliant repairs

By filing these claims, certified shops ensure that your vehicle is repaired completely and according to manufacturer standards—not just patched based on an initial surface-level estimate.

This line graph tracks the rising percentage of collision repair claims requiring supplemental estimates from 2018 to 2024. As vehicles become more complex, supplements are now part of the standard repair process.

Source: CCC Intelligent Solutions and Mitchell International, 2018–2024

A supplement may temporarily pause repairs while approval is granted, but it ensures no shortcuts are taken—and that you’re not left paying for overlooked repairs out of pocket.

OEM vs. Aftermarket Parts: What You Need to Know

One of the biggest sources of disagreement between insurance companies and body shops is the type of parts used for repairs. Insurers tend to favor aftermarket or recycled parts to reduce costs, while certified body shops prefer OEM (Original Equipment Manufacturer) parts to ensure safety, fit, and performance.

According to CCC Intelligent Solutions’ 2023 data, about 35.6% of all parts used in insurance-paid repairs are non-OEM, including aftermarket, recycled, and remanufactured parts. Meanwhile, body shops—especially those certified by vehicle manufacturers—prioritize OEM parts to meet strict repair standards.

Pros of OEM Parts:

- Exact Fit: OEM parts are designed specifically for your vehicle, reducing fitment issues

- Better Safety: OEM parts maintain the structural integrity of the vehicle in the event of another collision

- Preserves Warranty: Some aftermarket parts may void your manufacturer’s warranty

- Consistent Appearance: Paint finish, materials, and alignment match the original factory look

Risks with Non-OEM Parts:

- Variable Quality: Aftermarket parts vary in performance and durability depending on the manufacturer

- Fitment Issues: Recycled or remanufactured parts may not align perfectly, especially on newer vehicles

- Reduced Vehicle Value: Improper repairs using non-OEM parts can reduce trade-in or resale value

This pie chart breaks down the use of OEM vs. non-OEM parts in insurance-paid repairs. It shows that while OEM parts still dominate, a significant portion includes aftermarket, recycled, or remanufactured parts—especially in insurer-written estimates.

Know Your Rights in California

When comparing insurance vs. body shop estimates, California drivers are in a strong position—thanks to some of the most protective auto repair laws in the U.S. These laws exist to ensure you receive safe, complete, and fair repairs, not just cheap fixes designed to save insurers money.

Here’s what you need to know:

Your Key Rights (Backed by California Law)

| Your Right | What the Law Says | 2024 Update |

|---|---|---|

| Choose Your Own Repair Shop | Insurance Code §758.5 – Insurers can recommend shops, but can’t force you to use one | Over 600 complaints were filed in 2023 for “steering” attempts by insurers (FindLaw) |

| Know What Parts Are Used | 10 CCR §2695.8 – Insurers must tell you if your estimate includes non-OEM (aftermarket or recycled) parts | The CA Dept. of Insurance received hundreds of complaints for non-disclosed parts (Cornell Law) |

| Demand OEM-Quality Parts | Non-OEM parts must match OEM in quality, fit, and safety—or insurers must cover OEM | Several enforcement actions were taken in 2023 for non-compliant parts (Cornell Law) |

| Repairs Must Restore Safety | Shops must return your car to pre-accident condition—including safety systems and structural integrity | Increasing dispute cases prompted state-led audits in late 2023 (BAR Data) |

| File a Complaint | You can report unfair treatment to the California Department of Insurance | Thousands of complaints filed each year; top categories include body work, denied OEM parts, and estimate issues (CA DOI) |

What the Data Shows

To understand the scope of the issue, consider these recent statistics:

-

First, there was a 10.6% increase in California auto repair complaints at the end of 2023 compared to the same period in 2022.

-

In particular, the top complaint areas included auto body work, general maintenance issues, and the use of denied or non-OEM parts.

-

Furthermore, 63% of insurance estimates resulted in supplements once body shops performed detailed inspections and discovered hidden damage.

-

Lastly, over 35% of insurer-written estimates included non-OEM parts without properly disclosing them to the vehicle owner.

Why This Matters in Insurance vs. Body Shop Estimates

Given this data, it’s clear that the difference between insurance vs. body shop estimates is more than just numbers—it’s about quality, safety, and transparency.

-

While insurance adjusters often focus on minimizing costs, they may write estimates that skip essential procedures or rely on cheaper, non-OEM parts.

-

In contrast, certified collision centers prioritize restoring your vehicle to factory specifications using OEM parts and approved repair methods.

What You Can Do

Understanding your rights puts you in control of the repair process—not your insurance company. Here are a few key steps you can take to protect your vehicle and your peace of mind:

-

First, push back if your insurer tries to steer you toward a specific repair shop. You have the legal right to choose where your car is repaired.

-

Next, request OEM parts and make sure your repair shop follows the proper manufacturer procedures for safety and quality.

-

Finally, if you experience unfair treatment or your insurer insists on using substandard parts or shortcuts, file a complaint with the California Department of Insurance.

Bottom Line

At the end of the day, you don’t have to settle for shortcuts. California law gives you the legal right to demand high-quality, safe repairs—even when insurance vs. body shop estimates don’t match. Use that power to make informed decisions, insist on proper repairs, and protect the long-term safety and value of your vehicle.

Final Thoughts: Why Insurance vs. Body Shop Estimates Often Don’t Match

In the debate over insurance vs. body shop estimates, lower isn’t always better. If the insurance quote seems suspiciously low, there’s likely a reason. Insurance companies aim to control costs and process claims quickly. In contrast, certified body shops focus on safety, accuracy, and restoring your car to its pre-accident condition using proper procedures and OEM parts.

Instead of accepting the first number your adjuster gives you, take the time to compare. Relying solely on an insurance estimate may leave critical damage unrepaired, compromise your vehicle’s safety, or cost you more later when problems resurface. On the other hand, certified shops uncover hidden issues, document all damage, and use approved materials to ensure long-term safety and performance.

Key Takeaways

-

Don’t settle for the lowest estimate—request a full inspection from a certified repair facility

-

Most insurance estimates require supplements once hidden damage is revealed

-

You have the legal right to choose your repair shop and demand proper repairs

-

Certified shops prioritize safety, transparency, and long-term value over shortcuts

Ultimately, your body shop wants to repair your car the right way. The insurance adjuster wants to save money. That’s why their estimates don’t always align. In the end, your safety should come first—not your insurer’s budget.

What You Should Do Next

- Ask for a detailed, line-by-line estimate from a certified collision shop

- Let them handle the supplement process and communicate with your insurer

- Know your rights as a consumer, especially if you live in California

When faced with a decision between insurance vs. body shop estimates, choose the shop that puts your safety, your repair, and your rights first.

Need Accurate Estimates? Choose Premier Coach Auto Collision

When accuracy matters, Premier Coach Auto Collision delivers certified expertise you can trust. We’re proudly certified by Tesla, BMW, Porsche, Mercedes-Benz, and many more. Although we work with all major insurers, our commitment is to you—not the insurance company. Instead of cutting corners, we focus on repairing your vehicle the right way, using factory-correct procedures every time.

To begin, we perform a full visual inspection and teardown to find damage that insurance adjusters often overlook. Next, we develop a detailed, line-by-line estimate based on OEM guidelines and submit it directly to your insurer. Throughout the process, we handle all communications, ensuring transparency and full repair coverage from start to finish.

Why Choose a Certified Collision Shop Like Premier Coach Auto Collision?

Here’s what sets us apart from standard repair options:

-

✅ OEM Parts Only – Ensures proper fit, finish, and vehicle safety

-

✅ Thorough Inspections – Teardowns reveal hidden structural or electronic issues

-

✅ Certified Technicians – Trained to follow manufacturer-specific repair procedures

-

✅ ADAS & Safety Recalibrations – Keeps critical systems functioning as designed

-

✅ Accurate Paint Matching – Restores your car’s factory finish and appearance

-

✅ Insurance Claim Assistance – We manage supplement claims and paperwork on your behalf

-

✅ No Shortcuts – Every step aligns with strict OEM requirements

-

✅ Protects Vehicle Value & Warranty – Maintains resale value and preserves factory warranties

In short, we don’t just fix what’s visible—we restore your vehicle completely, the way the manufacturer intended.

Thousand Oaks | 805-373-7366

Camarillo | 805-389-9574